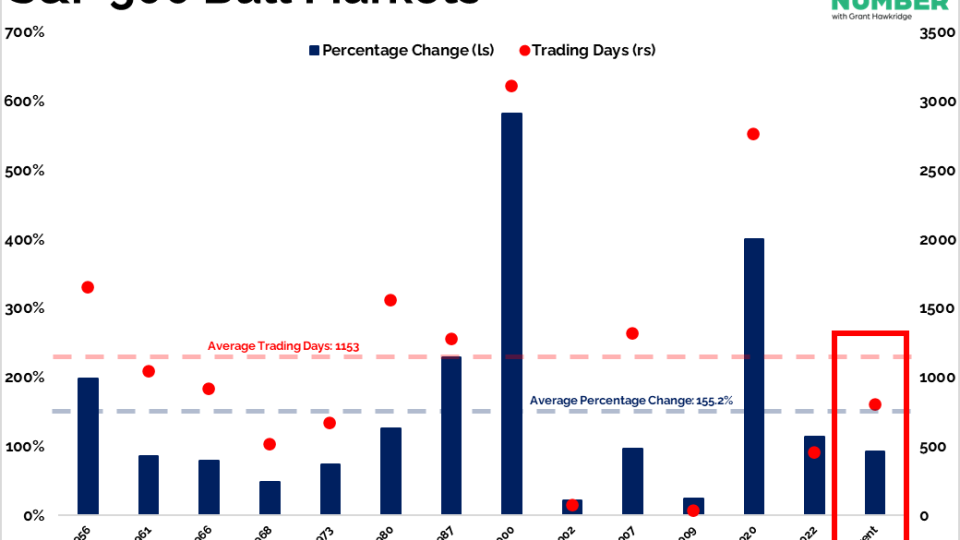

Grant Hawkridge 802 Days In, And This Bull Market Is Still Below Average ⏱️ Today's number is... 802 The current S&P 500 bull market has been running for 802 trading days. Here’s the chart: Let's break down what the chart shows: The chart displays S... December 24, 2025 Search Displaying 9001 - 9024 of 20169 Sean McLaughlin Collaborative Profits Strazza and I have been having fun discussing options stuff on Twitter Spaces over the past few weeks. Even our friend Brian Lund (@bclund) has... April 4, 2023 All Options ASC Patrick Dunuwila Daily Chart Report 📈 Tuesday, April 4th, 2023 April 4, 2023 The Chart Report Daily Chart Report Front Top Content Featured Stories JC Parets Swing Trader Pro: Afternoon Briefing (04-04-2023) From the Desk of Kimmy Sokoloff That was a healthy contraction today. I would think we still need more of a pull-in, but time will tell. April 4, 2023 Stocks Swing Trader Pro Newsletter Patrick Dunuwila Chart of the Day - Tuesday, April 4th, 2023 April 4, 2023 The Chart Report Commodities Gold TCR Chart of the Day $GLD $GOLD $GC_F $XAU Sean McLaughlin [Options P2P] Adjusted USO Position We've adjusted a position in the Paid-to-Play portfolio today: April 4, 2023 Options Paid to Play Paid To Play Members Only Sean McLaughlin [Options P2P] Trade Alert: Closed XLU at Profit Target We had a resting GTC order filled at our profit target in the Paid-to-Play portfolio today: April 4, 2023 Options Paid to Play Paid To Play Members Only JC Parets It would be weird Asset prices trend. We know this. We all have the data. Just because some (most)... April 4, 2023 Stocks ASC ASC Chart of the Day JC Parets Cormorant Likes BMEA Today’s most significant insider transaction report is a Form 4 filing by Cormorant Asset Management. The firm revealed a purchase of $12 million in Biomea Fusion $BMEA. April 4, 2023 Stocks Strazza The Hot List JC Parets Swing Trader Pro: Morning Briefing (04-04-2023) From the Desk of Kimmy Sokoloff Another gap higher this morning for the indices. We might hit $SPY 421 quicker than thought if we keep up this pace. April 4, 2023 Stocks Swing Trader Pro Newsletter JC Parets [Premium] Monthly Charts Strategy Session April 2023 This is the video recording of our April 3rd Monthly Charts Live Strategy Session April 3, 2023 All Star Charts Premium Stocks Currencies Commodities Interest Rates Conference Call bonds ASC Video Members Only Ian Culley [Video] Gold Rush: Risk Appetite Increases Gold finished the month within ten dollars of a new all-time high on a monthly closing basis. It's an impressive feat by any standards, but even more so considering March is the weakest month of the year from a seasonal perspective. ... April 3, 2023 All Star Charts Premium All Star Charts Gold Rush ASC Gold Ian Gold Rush Video Members Only Alfonso De Pablos, CMT Follow the Flow (04-03-2023) From the Desk of Steve Strazza @sstrazza and Alfonso Depablos @Alfcharts This is one of our favorite bottom-up scans: Follow the Flow. In this note, we simply create a universe of stocks that experienced the most unusual options... April 3, 2023 All Star Charts Premium Premium Stocks ASC Strazza Follow The Flow Alfonso Members Only Ian Culley Miners Break Out as Gold Approaches a New All-Time High From the Desk of Ian Culley @IanCulley I thought March was supposed to be a seasonally weak period for gold. I guess I was wrong... April 3, 2023 All Star Charts Premium All Star Charts Gold Rush ASC Gold Ian Gold Rush Members Only Patrick Dunuwila Daily Chart Report 📈 Monday, April 3rd, 2023 April 3, 2023 The Chart Report Daily Chart Report Front Top Content Featured Stories JC Parets Swing Trader Pro: Afternoon Briefing (04-03-2023) From the Desk of Kimmy Sokoloff It was a slow day for the market, and then, late in the day, we started to ramp higher. I'd think $QQQ... April 3, 2023 Stocks Swing Trader Pro Newsletter Alfonso De Pablos, CMT Under the Hood (04-03-2023) From the Desk of Steve Strazza @Sstrazza. Welcome back to Under the Hood, where we'll cover all the action for the week ended March 31, 2023. This report is published bi-... April 3, 2023 All Star Charts Premium Premium Stocks ASC Strazza Under The Hood Grant Members Only Sean McLaughlin [Options Premium] McDonald's Just Put "Rolls" on the Menu McDonald's just put "300-dolla-rolls" on the menu. Sweet and delicious. Limited time offer. Many of you know that my all time favorite options trades are simple long calls on stocks making new all-time highs. And when you add in a big round... April 3, 2023 All Star Options Options Options Premium Members Only Ian Culley Miners Break Out as Gold Approaches a New All-Time High From the Desk of Ian Culley @IanCulleyI thought March was supposed to be a seasonally weak period for gold.I guess I was wrong.Instead of rolling over, gold almost posted double-digit returns last month, while the higher... April 3, 2023 ASC Gold Rush Report Patrick Dunuwila Chart of the Day - Monday, April 3rd, 2023 April 3, 2023 The Chart Report Frank Cappelleri TCR Chart of the Day $OEF Sean McLaughlin [Options P2P] Adjustment to XLE Position We've adjusted a position in the Paid-to-Play portfolio today: April 3, 2023 Options Paid to Play Paid To Play Members Only JC Parets Your Leaders Are Leading I've argued for years that the Dow Jones Industrial Average is the ... April 3, 2023 Stocks ASC breadth JC Parets Ares Management Reveals Another FYBR Purchase Today’s most significant insider transaction report is a Form 4 filing by Ares Management. Ares revealed an additional purchase of roughly $2.9 million in Frontier Communications... April 3, 2023 Stocks Strazza The Hot List JC Parets Swing Trader Pro: Morning Briefing (04-03-2023) From the Desk of Kimmy Sokoloff Happy April... And what a move the market has made! April 3, 2023 Stocks Swing Trader Pro Newsletter Patrick Dunuwila The Buzz 🐝 Week 5 Welcome to The Buzz! Our mission at The Chart Report is to highlight ideas from the best traders and technicians on social media. Now, we’re taking this concept one step further and tapping into the... April 2, 2023 The Chart Report: Private Access Members Only Pagination Back 1 … Page 372 Page 373 Page 374 Page 375 Page 376 Page 377 Page 378 Page 379 Page 380 … 841 Next Recent Episodes December 23rd December 23, 2025 The Open Bar Buying Some Tech December 23, 2025 Hosted by Steve Strazza The Morning Show How Bout Them Banks? December 23, 2025 Hosted by Spencer Israel JC Parets Steve Strazza With special guest(s) Kenny Glick Phil Pearlman Chart Request Live Bring Your Tickers! We Will Break Them Down Live December 22, 2025 With special guest(s) Sam Gatlin Alfonso De Pablos, CMT December 22nd December 22, 2025 The Morning Show Who Thinks We're In A Bubble? December 22, 2025 Hosted by Spencer Israel JC Parets Steve Strazza With special guest(s) Kenny Glick "Chart Kid" Matt Cerminaro Missed it? No problem!Replays of all our past episodes are always available in the episode archives. View Episode Archives

Grant Hawkridge 802 Days In, And This Bull Market Is Still Below Average ⏱️ Today's number is... 802 The current S&P 500 bull market has been running for 802 trading days. Here’s the chart: Let's break down what the chart shows: The chart displays S... December 24, 2025

Sean McLaughlin Collaborative Profits Strazza and I have been having fun discussing options stuff on Twitter Spaces over the past few weeks. Even our friend Brian Lund (@bclund) has... April 4, 2023 All Options ASC

Patrick Dunuwila Daily Chart Report 📈 Tuesday, April 4th, 2023 April 4, 2023 The Chart Report Daily Chart Report Front Top Content Featured Stories

JC Parets Swing Trader Pro: Afternoon Briefing (04-04-2023) From the Desk of Kimmy Sokoloff That was a healthy contraction today. I would think we still need more of a pull-in, but time will tell. April 4, 2023 Stocks Swing Trader Pro Newsletter

Patrick Dunuwila Chart of the Day - Tuesday, April 4th, 2023 April 4, 2023 The Chart Report Commodities Gold TCR Chart of the Day $GLD $GOLD $GC_F $XAU

Sean McLaughlin [Options P2P] Adjusted USO Position We've adjusted a position in the Paid-to-Play portfolio today: April 4, 2023 Options Paid to Play Paid To Play Members Only

Sean McLaughlin [Options P2P] Trade Alert: Closed XLU at Profit Target We had a resting GTC order filled at our profit target in the Paid-to-Play portfolio today: April 4, 2023 Options Paid to Play Paid To Play Members Only

JC Parets It would be weird Asset prices trend. We know this. We all have the data. Just because some (most)... April 4, 2023 Stocks ASC ASC Chart of the Day

JC Parets Cormorant Likes BMEA Today’s most significant insider transaction report is a Form 4 filing by Cormorant Asset Management. The firm revealed a purchase of $12 million in Biomea Fusion $BMEA. April 4, 2023 Stocks Strazza The Hot List

JC Parets Swing Trader Pro: Morning Briefing (04-04-2023) From the Desk of Kimmy Sokoloff Another gap higher this morning for the indices. We might hit $SPY 421 quicker than thought if we keep up this pace. April 4, 2023 Stocks Swing Trader Pro Newsletter

JC Parets [Premium] Monthly Charts Strategy Session April 2023 This is the video recording of our April 3rd Monthly Charts Live Strategy Session April 3, 2023 All Star Charts Premium Stocks Currencies Commodities Interest Rates Conference Call bonds ASC Video Members Only

Ian Culley [Video] Gold Rush: Risk Appetite Increases Gold finished the month within ten dollars of a new all-time high on a monthly closing basis. It's an impressive feat by any standards, but even more so considering March is the weakest month of the year from a seasonal perspective. ... April 3, 2023 All Star Charts Premium All Star Charts Gold Rush ASC Gold Ian Gold Rush Video Members Only

Alfonso De Pablos, CMT Follow the Flow (04-03-2023) From the Desk of Steve Strazza @sstrazza and Alfonso Depablos @Alfcharts This is one of our favorite bottom-up scans: Follow the Flow. In this note, we simply create a universe of stocks that experienced the most unusual options... April 3, 2023 All Star Charts Premium Premium Stocks ASC Strazza Follow The Flow Alfonso Members Only

Ian Culley Miners Break Out as Gold Approaches a New All-Time High From the Desk of Ian Culley @IanCulley I thought March was supposed to be a seasonally weak period for gold. I guess I was wrong... April 3, 2023 All Star Charts Premium All Star Charts Gold Rush ASC Gold Ian Gold Rush Members Only

Patrick Dunuwila Daily Chart Report 📈 Monday, April 3rd, 2023 April 3, 2023 The Chart Report Daily Chart Report Front Top Content Featured Stories

JC Parets Swing Trader Pro: Afternoon Briefing (04-03-2023) From the Desk of Kimmy Sokoloff It was a slow day for the market, and then, late in the day, we started to ramp higher. I'd think $QQQ... April 3, 2023 Stocks Swing Trader Pro Newsletter

Alfonso De Pablos, CMT Under the Hood (04-03-2023) From the Desk of Steve Strazza @Sstrazza. Welcome back to Under the Hood, where we'll cover all the action for the week ended March 31, 2023. This report is published bi-... April 3, 2023 All Star Charts Premium Premium Stocks ASC Strazza Under The Hood Grant Members Only

Sean McLaughlin [Options Premium] McDonald's Just Put "Rolls" on the Menu McDonald's just put "300-dolla-rolls" on the menu. Sweet and delicious. Limited time offer. Many of you know that my all time favorite options trades are simple long calls on stocks making new all-time highs. And when you add in a big round... April 3, 2023 All Star Options Options Options Premium Members Only

Ian Culley Miners Break Out as Gold Approaches a New All-Time High From the Desk of Ian Culley @IanCulleyI thought March was supposed to be a seasonally weak period for gold.I guess I was wrong.Instead of rolling over, gold almost posted double-digit returns last month, while the higher... April 3, 2023 ASC Gold Rush Report

Patrick Dunuwila Chart of the Day - Monday, April 3rd, 2023 April 3, 2023 The Chart Report Frank Cappelleri TCR Chart of the Day $OEF

Sean McLaughlin [Options P2P] Adjustment to XLE Position We've adjusted a position in the Paid-to-Play portfolio today: April 3, 2023 Options Paid to Play Paid To Play Members Only

JC Parets Your Leaders Are Leading I've argued for years that the Dow Jones Industrial Average is the ... April 3, 2023 Stocks ASC breadth

JC Parets Ares Management Reveals Another FYBR Purchase Today’s most significant insider transaction report is a Form 4 filing by Ares Management. Ares revealed an additional purchase of roughly $2.9 million in Frontier Communications... April 3, 2023 Stocks Strazza The Hot List

JC Parets Swing Trader Pro: Morning Briefing (04-03-2023) From the Desk of Kimmy Sokoloff Happy April... And what a move the market has made! April 3, 2023 Stocks Swing Trader Pro Newsletter

Patrick Dunuwila The Buzz 🐝 Week 5 Welcome to The Buzz! Our mission at The Chart Report is to highlight ideas from the best traders and technicians on social media. Now, we’re taking this concept one step further and tapping into the... April 2, 2023 The Chart Report: Private Access Members Only

The Morning Show How Bout Them Banks? December 23, 2025 Hosted by Spencer Israel JC Parets Steve Strazza With special guest(s) Kenny Glick Phil Pearlman

Chart Request Live Bring Your Tickers! We Will Break Them Down Live December 22, 2025 With special guest(s) Sam Gatlin Alfonso De Pablos, CMT

The Morning Show Who Thinks We're In A Bubble? December 22, 2025 Hosted by Spencer Israel JC Parets Steve Strazza With special guest(s) Kenny Glick "Chart Kid" Matt Cerminaro

{kind=link}