Busy morning of earnings with a little something for everyone as we try to figure out who, if anyone, is actually experiencing a recession as opposed to just talking about it all the time.

This morning saw a decent report from the dominant player in the dismal wedding-focused jewelry space in Signet, deep-discount treasure hunt chain Ollies and the magnificent Williams-Sonoma, stuck in the middle of a rare sell-off.

Let's grade them!

Report Card Rules:

All grades are subjective and relative to each company's reputation, messaging and likely appeal to Wall Street.

I don't much care about Q4. Does anything seem longer ago right now than last Christmas? Q1 reports in retail are all about setting expectations for the next year, establishing clear deliverables and highlighting any tailwinds or concerns.

TLDR: These stocks are all way off fairly recent highs. Anything better than whining about troubling economic headwinds and guiding to something hugely negative is a Beat at this point.

Let's start in the Mall!

Signet: B+

Signet slightly beat the guidance issued in January but missed the original Q4 guidance offered in December. Signet also lowered it's view for sales and net income for the coming year to slightly below existing analyst estimates.

Under normal circumstances this report would have gotten sold but Signet had a trump card (no pun intended): A New CEO with a Better Plan.

Shares aren't up 14% because of the trailing numbers. Signet is higher because expectations were low and new CEO JK Symancyk announced his presence with authority.

Symancyk doesn't "own" the prior results. He was an outside hire brought in last November. His job was to be coherent, focus on the parts of Signet Wall Street likes and make some vague but smart promises.

Symancyk has a declining core business (wedding/ diamonds) and a decent cash-flow business. Symancyk is promising buybacks and closing 10% of the stores. The new-new guidance for 2026 is a wide-range of possibilities (net income has a range of over 20%) on the low side of existing estimates.

But Signet didn't get worse for the first time in several quarters. Wall Street loves new CEO's with plans for a back-half recovery. Can the rally last? I'm not chasing it.

No Position

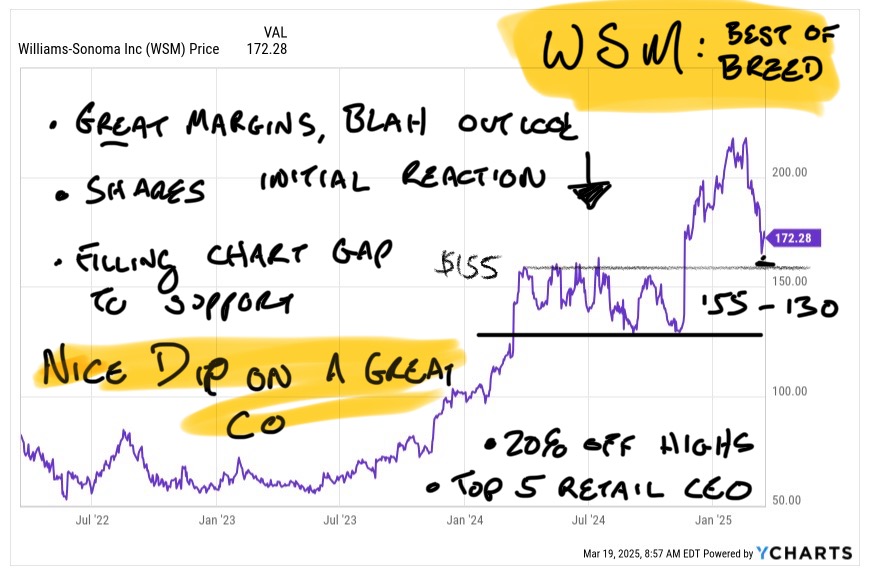

Williams-Sonoma: B-

William-Sonoma has one of the best CEO's in retail, a tremendous franchise and they've been on an absolute performance rip for the last few years, establishing it as a core brand rather than a niche' high-end offering.

As Abercrombie and others have shown, this isn't a market that wants to forgive high-performings expecting slower growth.

WSM is down pre-market and threatening to slip back to a range from the mid-150s to about $130 (where the stock was a year ago vs the peak at $217 in January:

This is a great brand down from $217 to $150 in 2 moths. I like the idea of buying this move MUCH more than chasing Signet higher. I doubt analysts defend a name in the very scary higher-end consumer space this week but you don't get many sales on WSM shares. Very bullish long term, terrified short term and have a trading idea for members.

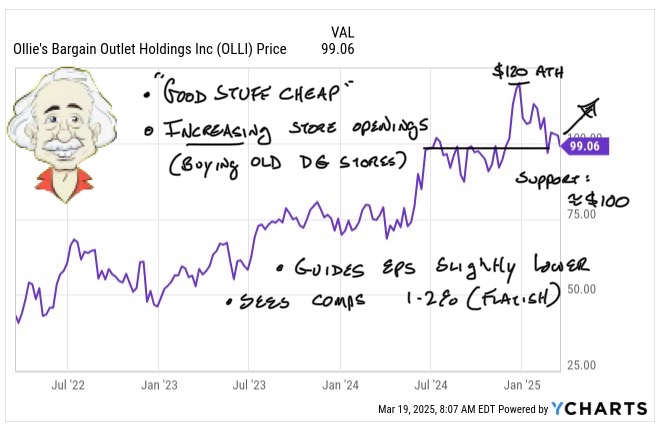

Ollie's Bargain Outlet: A-

Never heard of Olli's? Let me introduce you to Ollie's, where "good stuff is cheap"

There's a chance this is one of the better retail stories no one knows. Great chart, perfect target customer and the chart held $100 like an absolute champion.

Ollie's is up 10% very early. Good company meeting expectations perfectly. Ollie's also has a great narrative "Low-end TJX with a $6.6b market cap".

Ollie's is also sopping up retail real estate with the acquisition of 40 Big Lots with "below market rent... located in areas that have been serving value-oriented customers for many years".

Like Dick's, Ollies is going to bigger boxes while others pullback. Smart.

You need to have a subscription to access this content in full.

Log in or subscribe today to unlock new features and receive Member Benefits.