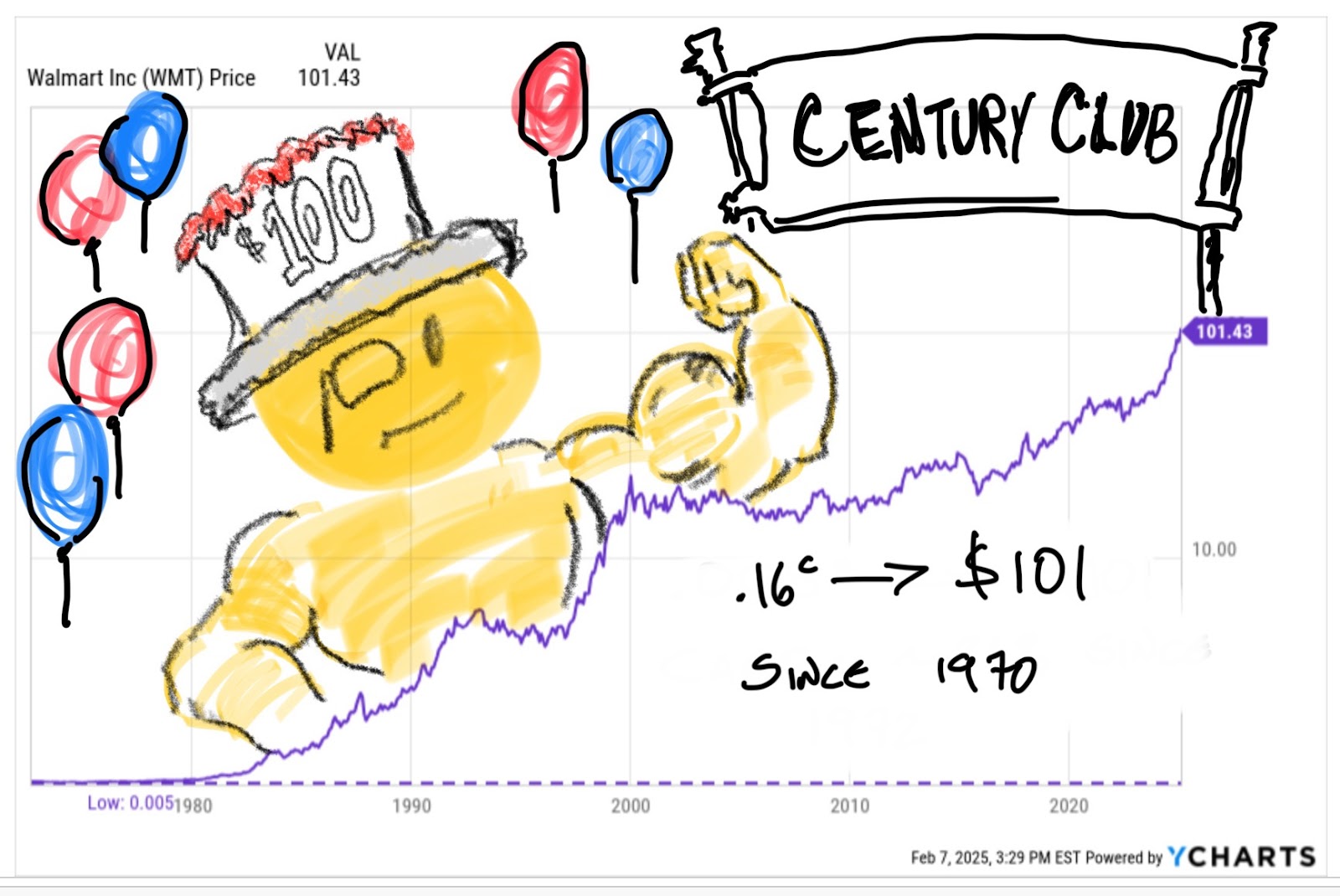

Walmart shares are up more than 80% in the last year despite single-digit revenue and earnings growth. Time to take gains on the World’s Largest Retailer?

I’ve been long shares of Walmart for the last 5 years. First the good news:

WMT is at all-time highs, having just ripped through Big Round Number resistance at $100 and forming one of those giddily unsustainable Upward to the Right charts you don’t see much in 65 year old retailers growing revenue at a single-digit rate.

Which is related to the bad-news. Walmart has rarely, if ever been this expensive by almost any measure. In the last 5 years Walmart shares are up 162%. In that same time frame revenue is up 26% and operating income has grown 22%. The latter numbers are surprising if not shockingly anemic.

At 41x trailing 12 months Walmart’s PE (“your grandpa’s ratio!”) is roughly 2x the historical average for the last 15yrs. In the last 12 months Walmart has gone from $56 to over $100 and the PE has moved from 25 to 42.

Walmart isn’t earning more money, it’s telling Wall St a better story.

“We’re Stealing the Amazon Playbook”

Last week I talked about buying the Amazon dip specifically because Amazon announced plans to increase spending. Amazon has gone from an online bookstore to company with at least 4 divisions big enough to be in the S&P 500 as stand alone businesses (Subscription Services, North American online sales, Third Party Services (which would be broken into shipping and back-end management), Physical Stores… seriously, “break up Amazon” is a whole different article).

What Amazon’s businesses have in common is they all tie back to the retail operation. In pursuit of faster delivery (better service) Amazon spent dumptrucks of money on order fulfillment and network efficiencies, which are now part of various services Amazon offers outside parties. So while Amazon chops out a decent but very “retail” margin of 6.4% on nearly $400b of North American retail AWS generates operating income of $40b on $107b in revenue.

And that’s what Wall Street is buying: The idea that Walmart will be able to use its massive top line to create its own handful of businesses which almost can’t help but have better margins than Walmart’s 5% profit from retail. For a retailer to have enough firepower to make those kind of investments it needs to have Scale and Brains. Walmart has both.

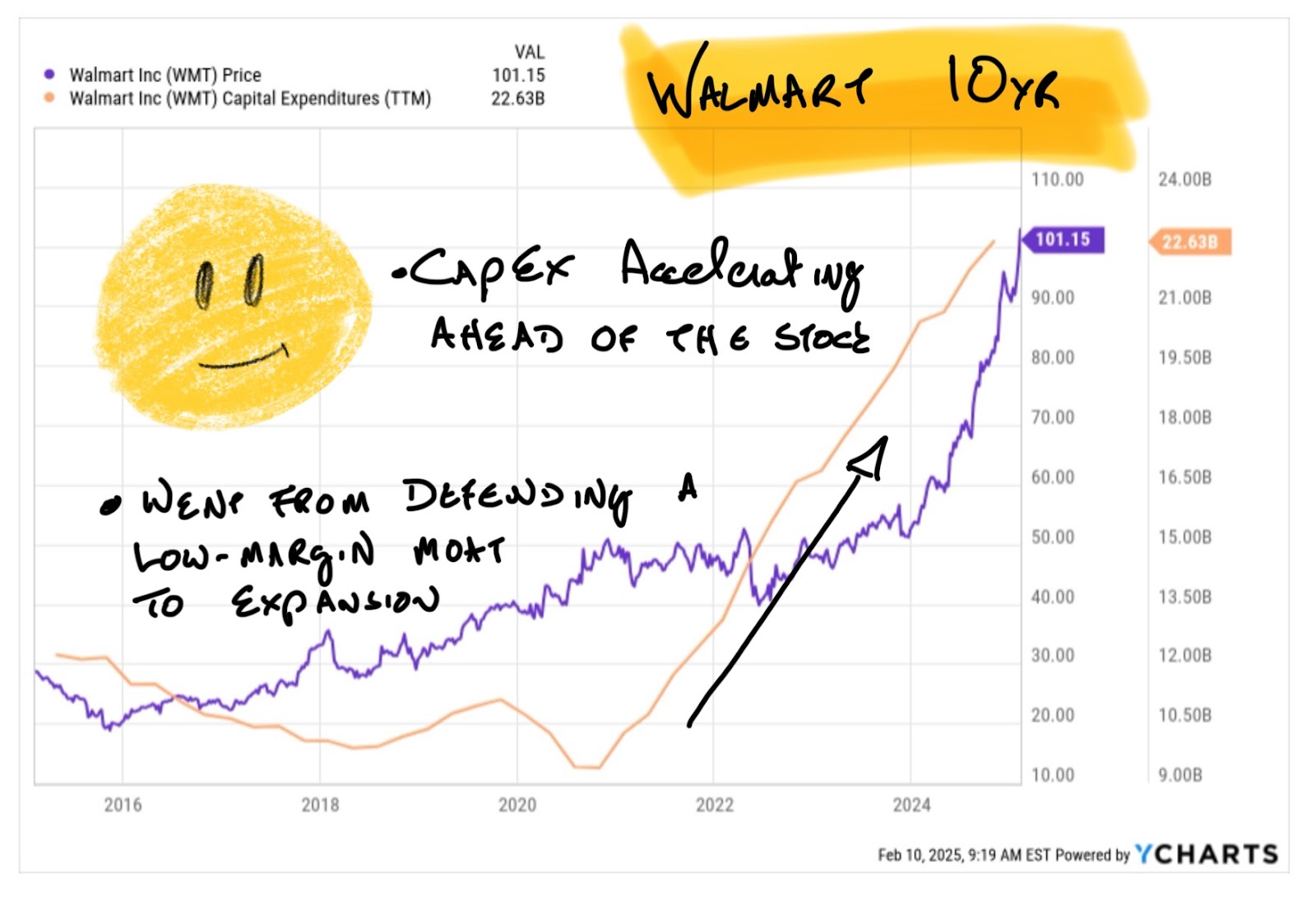

It’s not a coincidence that Walmart’s stock ripper resulted directly from the company turning it’s firehose of cash from buybacks and dividends to AI and online initiatives:

The price of a stock is determined by the net present value of the predictable cash flow stream plus whatever type of narrative bullshit a company can sell to Wall St. Bullshit isn’t necessarily bad. It just means not every initiative is going to be a banger and some of the flashier stuff is just a shiny object for analysts to look at while the company is doing wonkish things that actually ad value.

Eleven years ago Amazon announced drone deliveries on a very splashy 60 Minutes interview with Jeff Bezos. This year drone delivery will account for roughly zero percent of Amazon’s profits. That’s fine because the other infrastructure initiatives Amazon was putting in place at the same time have created about a trillion dollars of market value and Amazon shares are up >1000%.

No drones yet… just INSANE profits.

The Walmart Report Next Week

The bar is high for Walmart next week but not for reasons people think. I expect earnings to grow mid-single digits on upper single digit revenue growth. I’m willing to bet analysts want to see EPS kicking up over the course of the year to somewhere near 10%.

As a long-time shareholder who can’t justify the valuation on cash flow basis what I want is for Walmart to announce at least a 15% increase in CapEx for the next year. I want Walmart to throw cash at the pursuit of online initiatives, warehouse robotics and AI driven pricing. I want Walmart to tell me a story of becoming a compelling alternative to Amazon for third party merchants.

Walmart has a low-margin, no growth core business that has covered the earth already. Amazon has spent decades showing how to turn that kind of scale into an insanely lucrative flywheel. I want Walmart to steal that model. If they do a good job I’ll be able to stay long shares, and not take a cap-gains smack, for at least another year or more.