When it comes to retail dominance, few names carry as much weight as Costco Wholesale $COST.

For years, this company has been the gold standard for operational efficiency and customer loyalty.

They thrive in both inflationary and deflationary environments.

Whether consumers are stockpiling for uncertain times or looking for value in everyday essentials, it consistently delivers.

Membership growth remains steady, renewal rates are near all-time highs, and recurring revenue from fees continues to be one of the most underappreciated drivers of long-term value.

In the latest quarter, the company once again posted a double beat, and the market rewarded it with another move higher.

Despite broader concerns about slowing consumer spending, this business continues to prove it can grow, defend margins, and execute.

The market knows it. And the stock is acting accordingly.

So what else did we learn from Friday's earnings reactions? Let’s dive into the details.

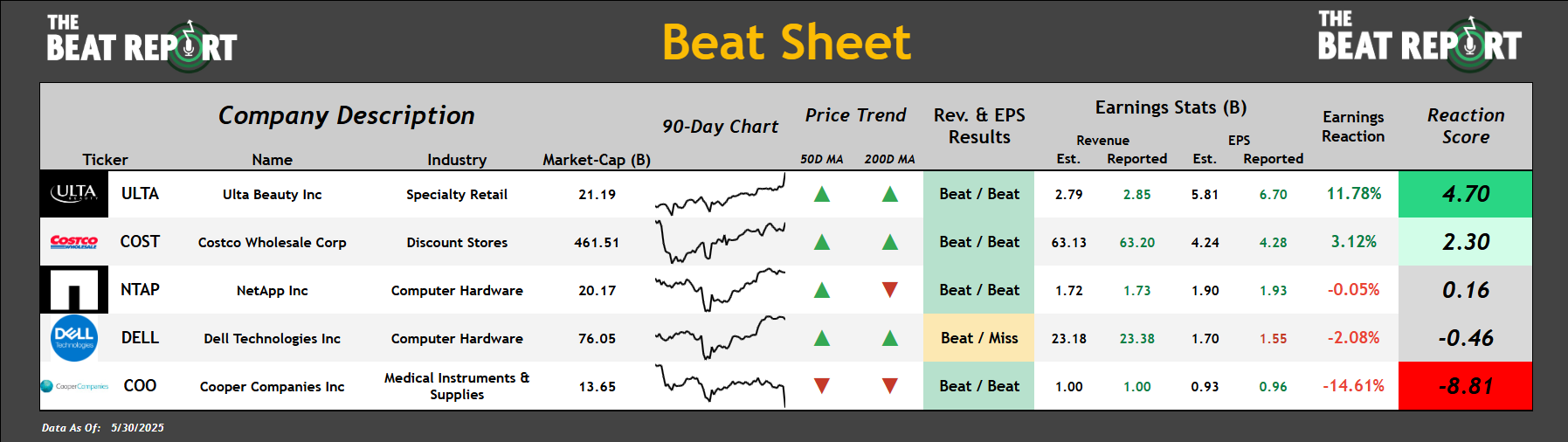

Here are the latest earnings reports from the S&P 500 👇

*Click the image to enlarge it

Ulta Beauty $ULTA had the best reaction score after reporting a double beat.

The company reported revenues of $2.85B, versus the expected $2.79B, and earnings per share of $6.70, versus the expected $5.81.

Cooper Companies $COO had the worst reaction score after reporting a double beat.

The company reported revenues of $1B, which met the market's expectations, and earnings per share of $0.96, versus the expected $0.93.

Now let's dive into the data and talk about what happened with these reports 👇

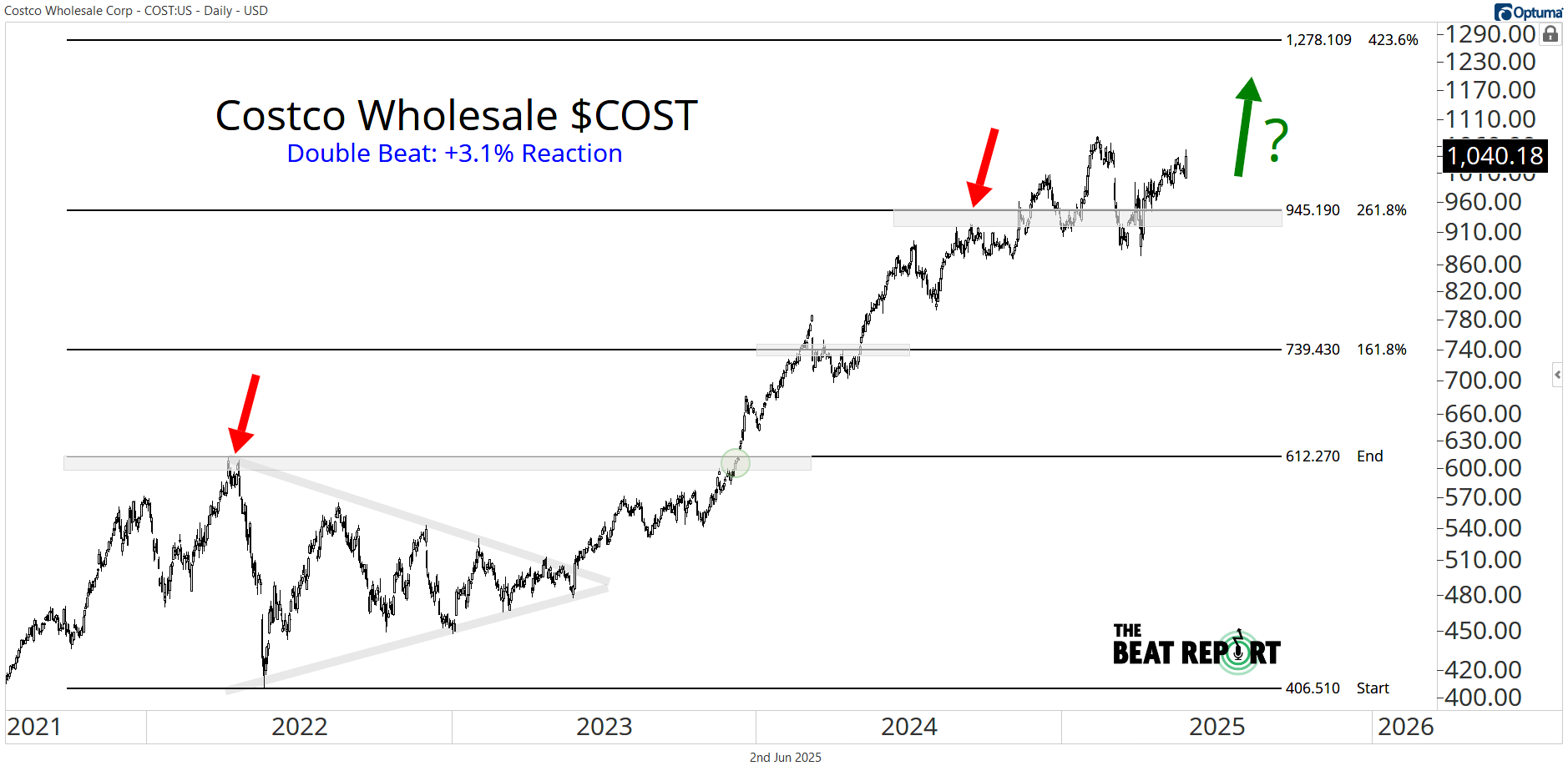

COST is flirting with new all-time highs after its earnings report:

Costco Wholesale rallied 3.1% after this earnings report, and here's why:

The company grew revenues by 8% year-over-year and net income by 13.2% over the same timeframe.

E-commerce revenue surged 14.8% Y/Y.

Paid memberships grew 6.8% (to 79.6M), and renewal rates stayed high at 92.7% in the US/Canada and 90.2% globally.

This company is one of the largest retailers in the U.S., and it continues to exceed the market's expectations.

Since the stock bottomed in 2022, its market capitalization has gone from $180B to nearly $500B.

It has also grown into the largest Consumer Staples Sector ETF $XLP component, at 10.3%.

We think they're positioned to continue dominating for years.

If COST is above 945, the path of least resistance will likely remain higher for the foreseeable future.

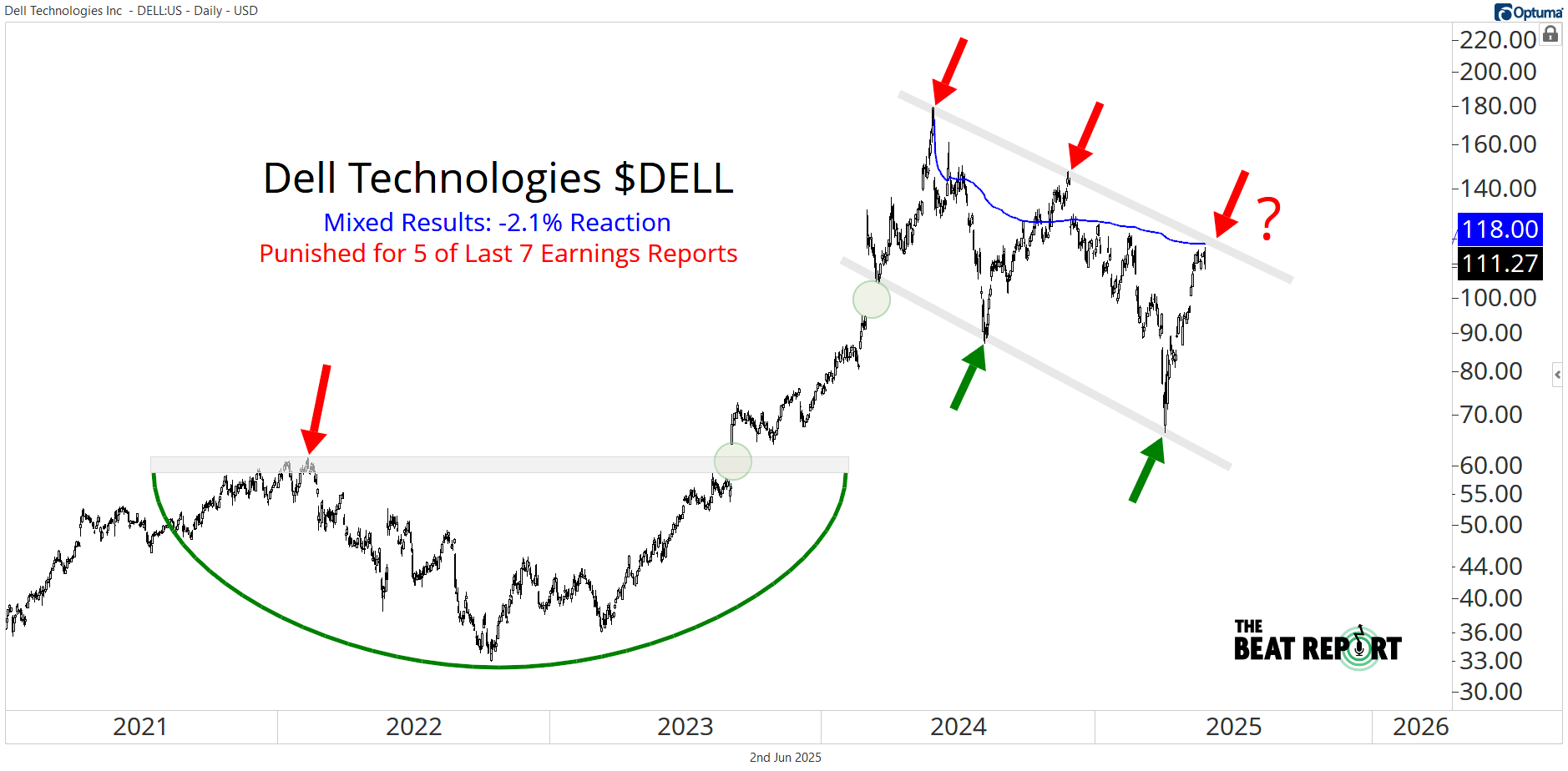

DELL has been punished for 5 of its last 7 earnings reports:

Dell Technologies fell 2.1% after this earnings report, and here's why:

Gross margin as a percentage of revenue declined to 21.6%, down from 22.4% a year earlier.

Profitability in the Client Solutions Group (CSG) is under notable pressure, as operating income fell 16% Y/Y and margin declined to 5.2%.

The management team reiterated its full-year revenue guidance but lowered its expectations for profitability.

A few years ago, this company soared in sympathy with the AI Revolution. Now, it's stuck in a massive range as its fundamental growth story is deteriorating.

The trend in negative earnings reactions highlights that the market has not been impressed recently.

As you can see on the chart, the price action has been incredibly messy for the last year, and we don't anticipate that changing soon.

If DELL is below 118, the path of least resistance will likely remain sideways to lower for the foreseeable future. The VWAP anchored to the all-time high is our line in the sand.

Thank you for reading.

- The Beat Report Team

P.S.: AI is moving fast. So is the tech reshaping how we live, work, and invest. In Godspeed, Riley Rosebee highlights the companies driving the future — and the price levels that matter right now.Follow Riley here.

If you find our content valuable, we would greatly appreciate it if you could shareit with your friends, family, and colleagues. Your help in spreading the word is invaluable in supporting our work. Thank you to all of you who share!