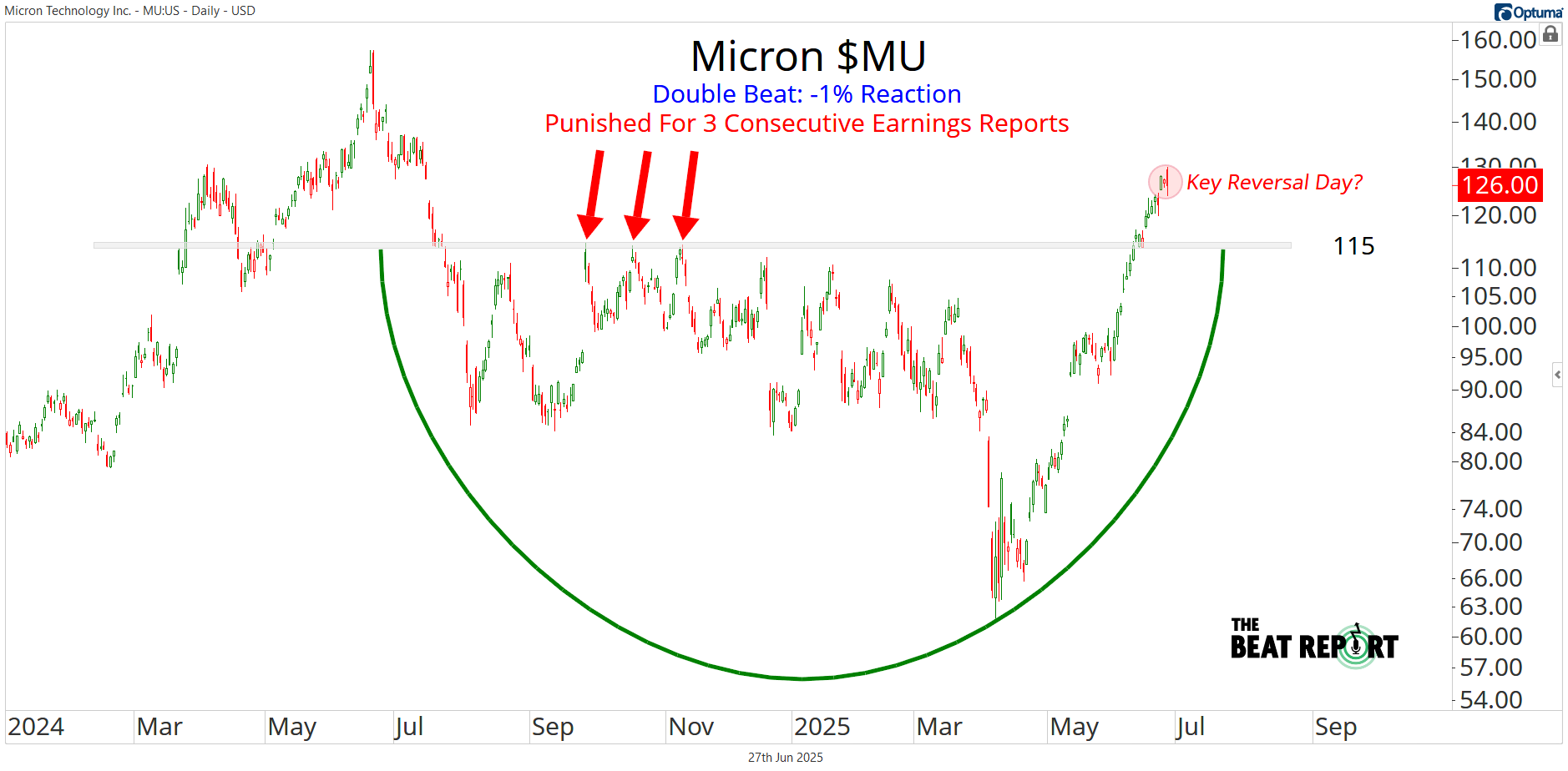

Micron $MU just delivered another double beat, but the market wasn’t impressed.

This marks the 3rd consecutive earnings report where investors have punished the stock despite strong headline numbers.

That’s a big red flag.

This company sits at the heart of the semiconductor supply chain, manufacturing DRAM and NAND memory chips that power everything from smartphones to servers.

Management has repeatedly identified 2025 and 2026 as major inflection points...

They’ve cited tighter supply conditions, a stronger pricing environment, and accelerating AI-driven demand as long-term tailwinds.

However, the market demands more than long-term promises... it wants margin expansion now.

As investors shift toward names demonstrating operating leverage today, the lack of upside follow-through in the stock is becoming increasingly difficult to ignore.

It’s still one of the most important players in the AI arms race.

However, until the strong fundamentals translate into bullish price action, it’ll remain stuck in neutral.

Will that change soon?

We'll see when they report again in 90 days.

So what else did we learn from yesterday's earnings reactions? Let’s dive into the details.

Here are the latest earnings stats from the S&P 500 👇

*Click the image to enlarge it

McCormick & Company $MKC had the best reaction score after reporting a double beat.

The company reported revenues of $1.66B, meeting the market's expectations, and earnings per share of $0.69, versus the expected $0.65.

Micron Technology $MU had the worst reaction score after reporting a double beat.

The company reported revenues of $9.30B, versus the expected $8.86B, and earnings per share of $1.91, versus the expected $1.60.

Now let's dive into the data and talk about what happened with these reports 👇

MKC has been rewarded for 6 of its last 7 earnings reports 🔥

McCormick rallied 5.3% after this earnings report, and here's why:

Despite cost pressures, the company delivered 10% adjusted operating income growth.

They're continuing to gain volume share across core categories, including spices and seasonings in the Americas and EMEA regions

In addition to the great quarter, the management team reaffirmed its forward guidance.

In a challenging environment for the Consumer Staples sector, this company is performing well relative to its peers.

The consistent positive market reactions to earnings indicate that the fundamentals have been improving for over a year.

The price is churning sideways below the VWAP, anchored to its all-time high in 2022.

This level is our line in the sand.

Below it, the path of least resistance is sideways to lower.

But if MKC is above our line in the sand, we want to give the bulls the benefit of the doubt.

MU has been punished for 3 consecutive earnings reports 🩸

Micron fell 1% after this earnings report, and here's why:

They reported record revenue of $9.30 billion, representing 15% sequential growth and 37% year-over-year growth.

Their data center business was particularly strong, with revenue more than doubling Y/Y and reaching a quarterly record.

While the management team provided good forward revenue guidance, the market was disappointed about the gross margin guidance.

If you find our content valuable, we would greatly appreciate it if you could shareit with your friends, family, and colleagues. Your help in spreading the word is invaluable in supporting our work. Thank you to all of you who share!